Do These Two Things to Build Better Credit

When you apply for a credit card, mortgage, car loan, or even a new cell phone account, there’s a good chance your credit score will play an essential role in the signup process. Credit scores and credit reports are vital tools lenders and other companies use to assess how likely you are to pay back a loan as agreed. This impacts your approval odds and interest rates once approved.

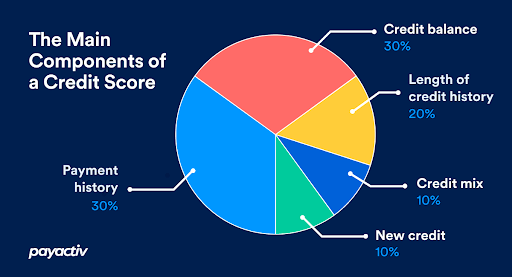

It’s easy to get overwhelmed trying to achieve a perfect credit score. Make things easier for yourself by staying focused on the two most important areas of your credit score calculation: payment history and your credit utilization ratio. These two factors that make up about two-thirds of your credit score, so let’s dive into how you can make the most of them to build your credit.

The Two Most Important Parts of Your Credit Score

The first factor you want to pay attention to is your payment history. Your payment history accounts for 35% of a FICO credit score.

The second factor is your credit utilization ratio, or how much you owe on credit cards and similar accounts, which makes up 30% of your score. That’s 65% of your score coming from these two areas alone, or nearly two-thirds of your credit score.

While other areas of your credit may also play an important role, focusing on these two is by far the most critical step you can take to build or repair your credit report, which in turn increases your credit score.

Building and Improving Your Payment History

Your payment history is the most important part of your credit score. There are no quick fixes or easy tricks to have a good payment history. That’s why it’s so important to always pay every credit-related bill by the due date, making at least the minimum payment.

Late payments and missed payments remain on your credit report for up to seven years. While a late payment or two may not be a big deal, a pattern of late payments causes serious harm to your credit score. Because it takes so long for late payments to drop off your credit report, it’s best to always pay on time.

To build better credit, commit to always making at least the minimum payment for every credit card and loan by the due date. If you have trouble remembering, you can use calendar reminders on your phone or automatic payments to help you stay on track.

To Do:

- Set up automatic payments for at least the minimum monthly payment

- Create calendar reminders for your payment due dates

- Sign up for payment reminders by email or text message from your lender

Keeping Credit Card Balances Low

The next most important area to focus on is your credit balances. Your credit score looks at the percentage of available credit used, and higher utilization lowers your credit score. While experts often suggest keeping below 20% to 30% of your credit limit, the best balance for your credit score is $0. This applies to other revolving credit accounts as well, including

If you have high credit balances, paying off your accounts is likely your quickest route to improved credit. However, as that’s often easier said than done, many savvy credit card users either avoid big balances to begin with or stick with a payment plan that will get them out of credit card debt for good.

As a perk for your efforts, you can save a small fortune on interest charges. When you pay off your entire credit card balance by the due date every month, you never have to pay any interest. If you can’t stick with a monthly payoff plan, it’s best to use credit cards sparingly or only for emergencies.

To Do:

- Pay off any outstanding credit card balances

- Keep your credit card balances low going forward

- Pay your entire credit card balance monthly by the due date

Other Key Factors In Your Credit Score

If you work on the two factors above, your credit score should improve over time. If your payment history and balances are doing well, the following factors are likely to follow suit. Credit history, credit account mix, and new accounts make up the last third of the credit score “pie”. Let’s dive into each of these smaller components and how they each can affect your credit score.

- Credit history length: The length of your credit history contributes 15% of your FICO score. To succeed here, avoid opening and closing accounts quickly. Keep accounts without an annual fee open as long as possible to build credit here.

- Credit account mix: Having multiple types of credit, such as a mix of credit cards and installment loans, shows lenders that you’re responsible with credit. A good mix of accounts makes up 10% of your credit score. However, most people shouldn’t open new credit accounts solely to improve their credit account mix.

- New accounts and inquiries: Applying for a new credit account results in a hard credit inquiry on your credit report, which has a minimal negative effect on your score. Opening new accounts also lowers your score temporarily. In most cases, this shouldn’t deter you from applying for and opening new accounts you actually need but should discourage you from opening new accounts without a specific goal.

Focus on Your Credit for the Long-Term

Your credit score and credit report are critical for your long-term financial success. The difference between an average credit score and an excellent one could save you tens of thousands of dollars when buying a home with a mortgage, among other benefits.

Because you can’t build or fix credit overnight, it’s essential to keep a long-term focus on your credit report and score. When you focus on always paying on time and maintaining low balances, and avoid opening and closing accounts frequently, you should be on track for an excellent credit score in the future.

Good luck!

Get Payactiv for your business

Learn how thousands of companies have improved their retention, recruitment, and engagement by offering Payactiv.

Request a Demo

Related Articles

Happy Financial Literacy Month! Financial literacy is an important skill that...

Credit cards are a valuable financial tool for renting a home or taking out a...

It’s easy to start a financial goal and give up a few months in, especially...