Payactiv Is Not a Bank, but You Can Bank on Us

Fintech companies like Payactiv have gotten a lot of attention lately from banks, especially from the traditional, brick-and-mortar kind of banks. It seems like a David and Goliath kind of story.

Except it’s really not.

How Payactiv Bridges the Gap Between Banking and Financial Services

Payactiv connects people’s earnings with a digital wallet and an exclusive ecosystem of discounts and services all in one app. We help people get access to their earned wages when they need them and give them more flexibility and insights with their spending, saving and budgeting.

Millions of people are sending their direct deposits to apps like Payactiv for the convenience of on-demand pay and digital financial services as opposed to traditional banks. The banks are noticing:

- FinTechs and digital banks captured 47% of new account openings in the first half of 2023.

- 75% of banks struggle to implement new payment solutions due to outdated infrastructure.

- 59% of bankers see their legacy systems as a major business challenge, describing them as a “spaghetti” of interconnected but antiquated technologies.

A Brief History of Banking

Banks, in a traditional sense, have existed since ancient times, and their primary purpose has always been to keep people’s money safe and to issue credit or loans. While this basic functionality is still true today, many things in the banking experience have changed dramatically.

While back in the day it was common to go to the bank to deposit checks and get cash, today people rarely have a need to go to the actual physical bank location, unless they are applying for a new account or a loan. Since the invention of the debit card in 1966 by the Bank of Delaware, banking has come a long way. Americans are not only making most of their purchases using debit cards today, but they are also going completely cardless with their smartphones by using digital wallets, such as the one from Payactiv.

Why Traditional Banks Fall Short for Many Workers

Waiting in line at the bank to deposit a check has become less and less common, much the same way as having a landline or a CD collection. It was okay back in the day, but now that we have smartphones that allow us to listen to music, make video calls, and transfer money with a touch of a button, who wants to spend their time at the bank?

With the evolution of the Internet came the online banking revolution as well. Initially only a few banks offered online banking but by 2006, it was offered by 80% of US banks. It wasn’t long before digital only or “neobanks” appeared and started changing the way we think about banking altogether.

Without the burden of operating costs associated with physical branches, digital-only banks focused on delivering better banking experiences through innovative technology. They were agile, and most importantly—they eliminated the annoying fees, like minimum balance requirements, overdraft fees, inactivity fees, and the like.

Some people worry if they can really trust these digital-only banks. It’s a fair question and one should always make sure that the business that you entrust your money with is legitimate and FDIC-insured. The reality is that most digital-only banks and fintechs, like Payactiv, are actually partnered with a traditional bank and card processor for all the back end processes and compliance. Because of this partnership, they are able to focus on the digital banking experience and deliver extraordinary new in-app financial services like bill management, peer-to-peer payments, and smart saving and budgeting tools.

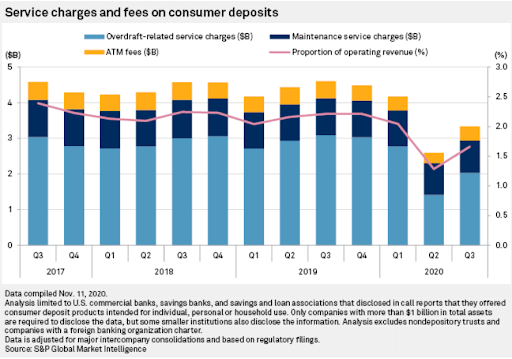

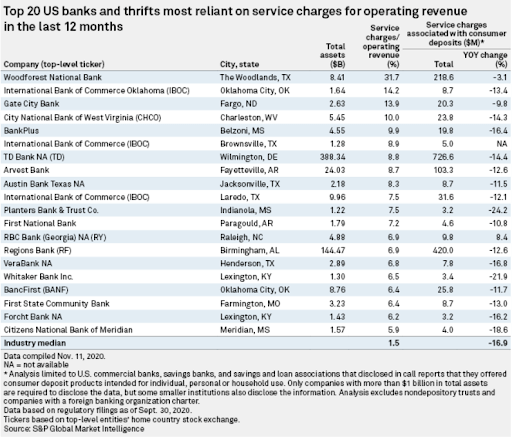

The Scandal of Bank Fees

Some mistrust in traditional banks is understandable:

- ATM fees are at an all-time high. The average total cost for using an out-of-network ATM is currently $4.77. This includes the average surcharge of $3.19 levied by ATM-operating banks, plus the average fee of $1.58 from one’s own bank for using an out-of-network ATM.

- Overdraft fees are on the rise. After declining for two years, the average overdraft fee has risen to $27.08 in 2024, up 1.7% from last year. The average nonsufficient funds (NSF) fee stands at $17.72.

- For interest checking accounts, the average minimum balance to avoid service fees has increased sharply. The average monthly fee for interest checking accounts is currently $15.45, with the average minimum balance to avoid monthly fees being $10,210 — up 18% from last year.

Payactiv: Supporting the Unbanked and Underbanked

Unfortunately, for some, even access to basic banking services is still not an option.

In 2023, 4.2% of U.S. households—representing about 5.6 million households—were unbanked, meaning nobody in the household had a checking or savings account with a bank or credit union:

- The unbanked rate changed little from 2021 (4.5%).

- Unbanked rates among Black, Hispanic, and American Indian or Alaska Native households remain several times higher than the unbanked rate among White households

- As in previous years, among all unbanked households, “Don’t have enough money to meet minimum balance requirements” was the most cited main reason for not having a bank account, followed by “Don’t trust banks.”

Digital bankings apps like Payactiv have eliminated archaic banking requirements along with the unnecessary fees and opened up doors to more people.

Payactiv’s Role in Providing Alternative Financial Services

In the U.S., 31% of consumers say they use cash less than they did 12 months ago. Nearly three-quarters express no concerns about moving to a cashless society, with 28% even reporting feeling awkward when paying with cash. This sentiment is especially strong among younger consumers, with almost half of those aged 18 to 34 feeling uncomfortable using cash.

Additionally, one-third of consumers said they use a digital-only bank in addition to their primary bank, pointing to a growing openness to non-traditional financial services and mobile banking offerings:

- 18% of consumers would consider moving all their banking to a digital-only option.

- 78% already use at least one financial provider outside their primary bank.

- 63% of U.S. consumers aged 18-34 saying they would consider getting financial services from non-traditional providers like tech companies, social media platforms or retailers.

While Payactiv doesn’t claim to be a bank, we are partnered with one and honored to provide some extraordinary financial services to millions of people and help them live the life they earned. So, it’s really a story where David and Goliath become friends and do some great things together.

To learn more about Payactiv’s services, get in touch with us, and let’s talk.

All content provided on Payactiv.com/financial-learning/ is for informational purposes only. Payactiv makes no representations as to the accuracy or completeness of any information on this site or found by following any link from this site. Payactiv will not be liable for any errors or omissions in this information nor for the availability of this information. Payactiv will not be liable for any losses, injuries, or damages from the display or use of this information.

Get Payactiv for your business

Learn how thousands of companies have improved their retention, recruitment, and engagement by offering Payactiv.

Request a Demo

Related Articles

Payday has never been static Today, it matters more than ever We’re excited...

Key takeaways: Automated cashless tips provide a secure and efficient way to...

The heart of every business is its employees, and these employees need to be...